Business credit cards offer some fantastic sign on bonuses and rewards. Business credit cards are meant for small and large business owners to charge and organize their business related expenses.

But does this mean you have to have a booming business making the big bucks to apply and be approved for one?

This post is part of my comprehensive guide to travel hacking where I go into detail about how I fly for free, book the cheapest flights, and how to be an overall better traveler!

Why apply for Business credit cards?

Most people think they can only apply for regular personal credit cards and are completely clueless about the world of business cards. The majority of good personal credit cards have a nearly identical business version of it. For example the following is just a small sample of the business credit card offerings out there.

When it comes to managing your business finances more efficiently, exploring options for online business banking can also provide added convenience and streamlined financial operations. Many financial institutions offer specialized online platforms tailored for businesses, providing features such as easy transaction monitoring, invoicing tools, and expense tracking to enhance overall financial management. As businesses increasingly embrace digital solutions, online business banking has become an integral part of ensuring financial success and operational efficiency.

- American Express Platinum vs American Express Platinum for Business

- Chase Sapphire Reserve vs Chase Ink Preferred

- Citi AAdvantage Platinum Select vs CitiBusiness AAdvantage Platinum Select

- AMEX Marriott Bonvoy vs AMEX Bonvoy Business

The best part? The Business card version of the card will usually have a sign on bonus that is almost identical. If the AMEX Delta Gold is offering 60,000 SkyMiles as a sign on bonus, the AMEX Delta Business Gold card will likely also be offering a 60,000 miles bonus.

In essence, the Business card world is another avenue to accrue points and miles. It is an integral part of my credit card repertoire and the reason I can always fly for free.

It’s even common for people (myself included many times over), to apply for the personal and business versions of the same card at the same time.

For example, I recently applied for the AMEX Starwood Business Card, as well as the AMEX Starwood Personal Card. The Business version offered 35,000 SPG points (after spending $7,500 in 3 months) as a sign on bonus, and the Personal card offered 30,000 (after spending $3,000 in 3 months) for a total of 65,000 points on sign on bonus alone! This is worth ~$1,800 by The Points Guy’s latest valuations.

Do note that having too many new cards at once makes it tough to meet the minimum spend requirement unless you have that type of spending power. However, there are ways to generate artificial spend.

Do Business cards affect your credit report?

When you apply for a business credit card, the bank will make a hard inquiry into your credit report. This is like applying for any other credit card including personal credit cards. This will affect your credit score, but not in a overly detrimental way as I discuss in detail in my post about why opening up many credit cards does not kill your credit score.

As far as getting approved for a business credit card, the bank will look at your credit report/score and take into account the usual variables that they would with a personal credit card application. They also will factor in how much revenue your business generates into the equation.

However, once you get approved, the card does not appear in your personal credit report. What does this mean and why does this matter?

Business credit cards do not appear on your credit report

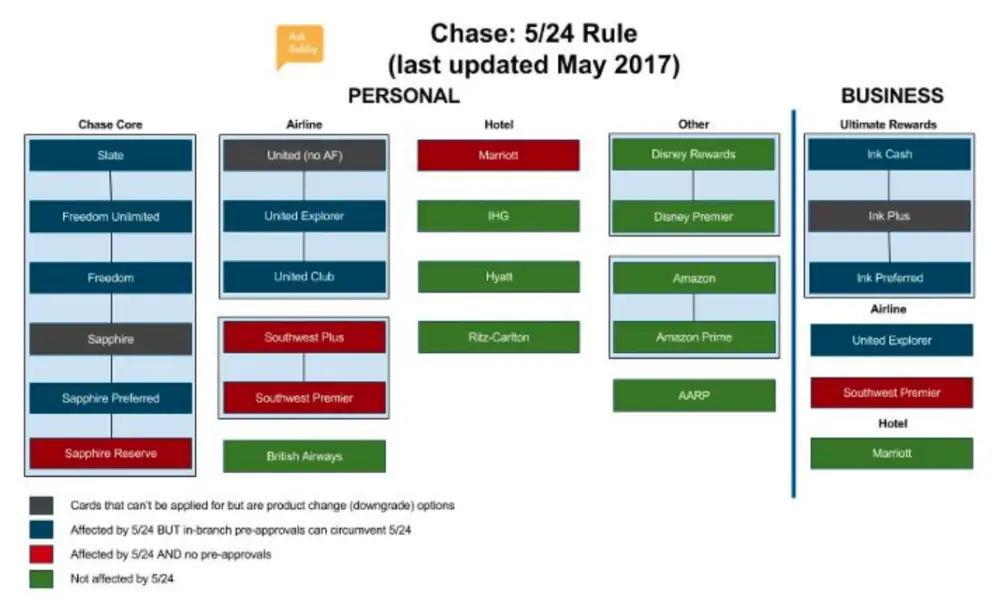

Once you are approved for the card, the vast majority of business cards do NOT appear on your credit report. This is one of the benefits of applying for business cards is that they do not show up on your personal credit report. This is especially important when applying for Chase credit cards that are subject to a 5/24 rule (5 cards within 24 months) maximum. This is especially important because Chase has the best business credit cards in the business so you’ll want to be under 5/24.

Business credit cards do not factor into your total credit utilization or your average age of credit. Missing payments on Business credit cards also do not have an effect on your credit report (Although defaulting on payments might).

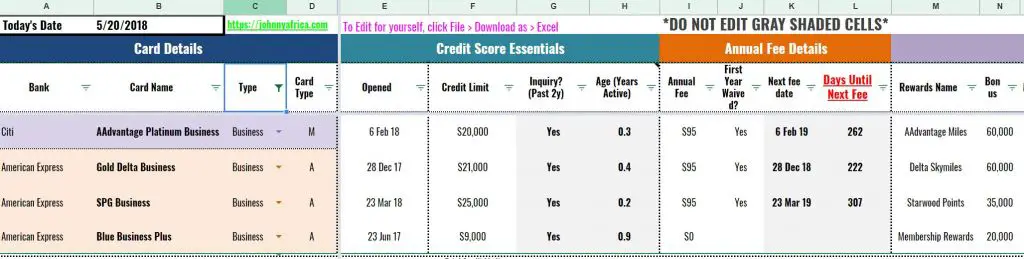

My current business card inventory

At any given moment, around half of my inventory is normally business credit cards. They do not appear on my credit report and allows me a fighting chance to get under the Chase 5/24 rule which is the bane of my existence. I track all my credit cards using my detailed credit card spreadsheet which has helped thousands of people reach the common goal of more travel!

As of June 2018, my business credit card inventory stands as such:

Only 4 cards at the moment (and I just got approved for the Chase Marriott Business) but I have canceled a few in the last year and plan to open at least 3 more business credit cards by the end of the year. From business credit cards, I’ve accumulated over a half million miles and points in the past few years.

How to apply for a business credit card?

If you’ve ever applied for a business credit card, you’ll see that the application is pretty straight forward. They ask basic questions about your business revenue and business industry, along with the standard credit card information like name, birth date, address, and social security number.

Most people think you need a traditional “brick and mortar” business like a store selling goods and services in order to qualify as a business. I am here to tell you that almost anything in life can qualify as a business. Whether you have a rental apartment, to selling old clothes on Ebay, to walking dogs. A business is after all, an entity that’s purpose is to make money. If you’re stuck on which “industry” your business falls under while filling out an application, just choose the other bucket and call it a day.

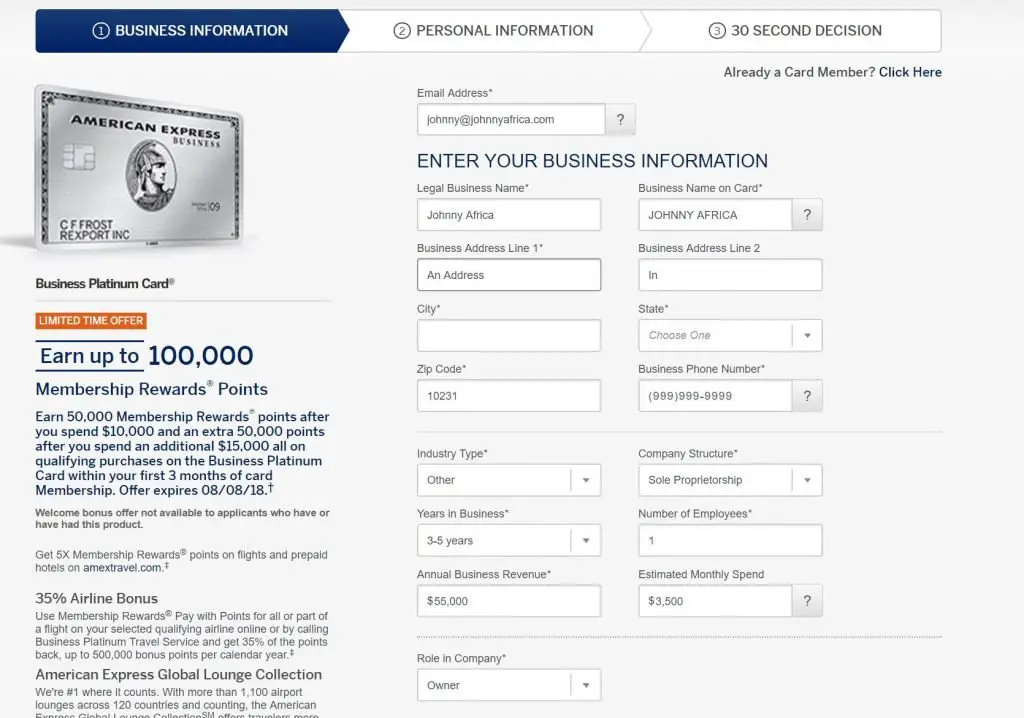

You can see from the image above how I go about filling out a business application for the AMEX Business Platinum Card.

My blog is a business

[mk_blockquote style=”line-style”]Blogging is a business too[/mk_blockquote]

For myself, my blog is a “business”. I didn’t create an app, nor am I generating income by conventional measures. Nevertheless, Johnny Africa generates a few thousand dollars a year so by definition, I am a business. While my “purpose” is not to make money whatsoever (I thoroughly just enjoy writing and documenting my travels), I just happen to generate income from it and therefore I am a business.

These business cards are geared towards “Small Business Owners” on all their marketing materials anyhow so don’t feel bad.

You don’t even need a business name

You can simply use your own name as the name of your business. Loads of people’s businesses are simply their name. Think of Doctors, law offices, etc. If you want the least amount of headache, especially with Chase credit card application, do the following:

- Use your personal name as as your business name

- Select Sole Proprietorship

- Use your SSN as your Tax ID

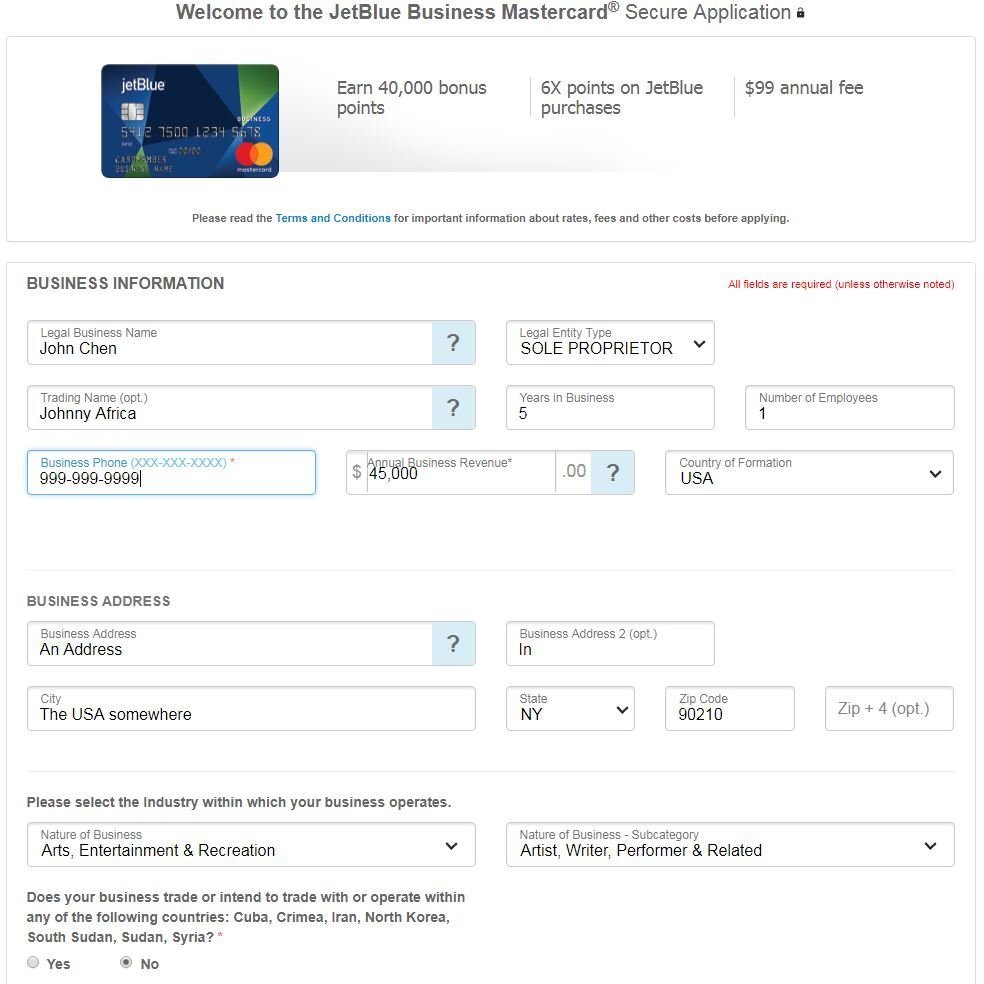

See the below example of filling out a Barclaycard Jetblue Business card application that’s offering 40,000 Jetblue points as a sign on bonus

What to report on Business Revenue

As for business revenue, always say your annual revenue is over $10,000. Yep I said it, just embellish your application and you’ll get approved. No one else will tell you this but this is the truth! To be on the safe side, I would put at least $25,000 in the annual revenue box in your application. Again, banks almost never take any steps to verify this information. This might seem morally wrong but just remember how much money these banks are making off poor folks with their 20%+ interest rates.

There is also an annual income box and here you can add your business revenue and your salary (if applicable) from your job.

Get an EIN as a Sole Proprietorship

If you own a business that you operate by yourself, you are a sole proprietorship. I am a sole proprietorship. Johnny Africa is a sole proprietorship. For every business application I do, I always select sole proprietorship. As such, I applied and have an EIN (Employer Identification Number). These are free to apply for and you can get one from your state government website very easily. It took me a few minutes to set up.

On credit card applications, there are usually two fields: Tax ID and Social Security Number. If you have an EIN and want to use it, you can put that in the Tax ID field and your SSN in the Social Security field. If you don’t have an EIN or do not want to use your EIN, you can also just use your SSN for the Tax ID and the SSN fields. Either method is fine.

For the really advanced churners, you can actually apply for two of the same business credit card. You may even consider the help of a business credit building program. Your first card would be with your SSN as the Tax ID and SSN as the Social Security number, and your second card would be with your EIN as your Tax ID and your SSN as the Social. This is considered two cards and you can get twice the sign up bonus. I will write a post about doing this in detail at a later point.

Different issuers require different things

Not all banks are the same. I find that AMEX and Barclays are some of the most lenient when it comes to issuing business cards. Citi is somewhere in the middle. Chase is notoriously difficult, and that is without even considering their 5/24 rule. Capital One is also not easy to get approval for. I’ve heard that Chase sometimes requires you to verify your business through financial statements but I have never had to go through this for myself.

What to do if you’re not approved right away?

It’s likely that you’ll not be approved right away. Often times, this just means they have an actual person looking at your application and it just takes a few days. Sometimes, they will actually call you to verify details of your business. If this happens and you do not have a confident business, make sure you practice and can answer simple questions like but not limited to the below:

- What type of business you have?

- How long have you been in business?

- How much money you made last year?

- How do you market your business?

- How much money you plan to make next year?

Other times, they might reject your application outright in which case you should call their credit reconsideration lines and ask the credit analyst if you can provide any details to have them reconsider your application. However, as long as you did everything I mentioned above, are below 5/24 if you’re applying for Chase cards, have a good credit score, then you should be fine.

So do you need a business to get business credit cards?

The truth of the matter is, the banks could take measures to verify your business like asking for financial statements but none of them do. They simply ask you for your business name, business structure, and revenue. The answers you give for those questions is totally up to you. The rest of the application which asks for your name, address, SSN, is all the same as a personal card application.

Since they don’t verify your business, you can totally just make up a business name and revenue number. I’ve instructed many of my friends to do the same and they have all been approved without a problem. So to answer the age old question do you need a business to get a business card?

No you do not need a business to apply for business credit cards.

I still think you should have some sort of business activity to apply for these cards just out of principal but I am here to set it straight that “technically”, you do not need one.

If you still don’t feel comfortable with applying for a business credit card without a business, just remember that anyone that sells anything at all for a profit can be considered a business. If you’re selling goods on eBay or Amazon on a semi-frequent basis, you are viewed as a business by the IRS. The income you receive needs to be reported on a tax return and you can therefore be considered a business!

Websites that need to be politically correct like The Points Guy (they receive a lot of money from the major banks) will give you some watered down answer like you need to have some sort of revenue generating business or hobby. They can’t completely exploit the system or be seen as promoting it. They are after all, directly paid by banks who are in the business of making money from issuing their credit cards.

What are the best business credit cards out there?

So now that you’ve learned that you don’t really need a real business to apply for business credit cards, what are the best cards available? Well this will always change as different banks have different deals at different times. My favorite place to keep track of the offerings is Doctor of Credit’s Business credit card offers page.

Largely, these cards have not changed in the past few years with how great their offerings are:

- Barclaycard Aviator Red Business

- Barclaycard Jetblue Plus Business

- Chase Ink Preferred

- Chase Ink Unlimited

- Chase Ink Cash

- Chase Marriott Business Premier

- AMEX Business Platinum

- AMEX Gold Business

- AMEX Business Gold Delta

- AMEX Business Platinum Delta

- Barclaycard AAviator Red Business

- Bank of America Alaska Mileageplan Business

- Citi AAdvantage Platinum Select Business

Thank you for providing such a helpful article on business credit cards! Really helped with understanding how to really open business cards

Glad it helped!

Thank you! Interesting information.

Just saying if you lie on an application and default you can go to jail.

great post! Quick question – What is your stance on putting personal expenses on business cards? I’ve heard different reasons for both sides, curious how you’ve approached it.

Hi Jack, I don’t differentiate at all. I just make sure to spend enougyh to hit the minimum requirement to get the sign on bonus. You will not be penalized or anything of the sort.

Got it, thanks for the reply.